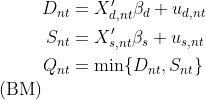

## The basic disequilibrium model

The basic model is the simplest disequilibrium model of the package as

it basically imposes no assumption on the market structure regarding

price movements (Fair and Jaffee 1972; Maddala and Nelson 1974). In

contrast with the equilibrium model, the market-clearing condition is

replaced by the short-side rule, which stipulates that the minimum

between the demanded and supplied quantities is observed. The

econometrician does not need to specify whether an observation belongs

to the demand or the supply side since the estimation of the model will

allocate the observations on the demand or supply side so that the

likelihood is maximized.

## The basic disequilibrium model

The basic model is the simplest disequilibrium model of the package as

it basically imposes no assumption on the market structure regarding

price movements (Fair and Jaffee 1972; Maddala and Nelson 1974). In

contrast with the equilibrium model, the market-clearing condition is

replaced by the short-side rule, which stipulates that the minimum

between the demanded and supplied quantities is observed. The

econometrician does not need to specify whether an observation belongs

to the demand or the supply side since the estimation of the model will

allocate the observations on the demand or supply side so that the

likelihood is maximized.

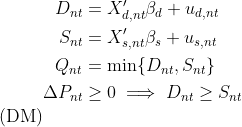

## The directional disequilibrium model

The directional model attaches an additional equation to the system of

the basic model. The added equation is a sample separation condition

based on the direction of the price movements (Fair and Jaffee 1972;

Maddala and Nelson 1974). When prices increase at a given date, an

observation is assumed to belong on the supply side. When prices fall,

an observation is assumed to belong on the demand side. In short, this

condition separates the sample before the estimation and uses this

separation as additional information in the estimation procedure.

Although, when appropriate, more information improves estimations, it

also, when inaccurate, intensifies misspecification problems. Therefore,

the additional structure of the directional model does not guarantee

better estimates in comparison with the basic model.

## The directional disequilibrium model

The directional model attaches an additional equation to the system of

the basic model. The added equation is a sample separation condition

based on the direction of the price movements (Fair and Jaffee 1972;

Maddala and Nelson 1974). When prices increase at a given date, an

observation is assumed to belong on the supply side. When prices fall,

an observation is assumed to belong on the demand side. In short, this

condition separates the sample before the estimation and uses this

separation as additional information in the estimation procedure.

Although, when appropriate, more information improves estimations, it

also, when inaccurate, intensifies misspecification problems. Therefore,

the additional structure of the directional model does not guarantee

better estimates in comparison with the basic model.

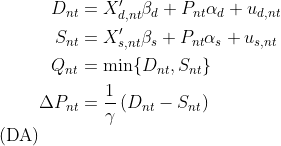

## A disequilibrium model with deterministic price dynamics

The separation rule of the directional model classifies observations on

the demand or supply-side based in a binary fashion, which is not always

flexible, as observations that correspond to large shortages/surpluses

are treated the same with observations that correspond to small

shortages/ surpluses. The deterministic adjustment model of the package

replaces this binary separation rule with a quantitative one (Fair and

Jaffee 1972; Maddala and Nelson 1974). The magnitude of the price

movements is analogous to the magnitude of deviations from the

market-clearing condition. This model offers a flexible estimation

alternative, with one extra degree of freedom in the estimation of price

dynamics, that accounts for market forces that are in alignment with

standard economic reasoning. By letting

approach zero, the equilibrium model can be obtained as a

limiting case of this model.

## A disequilibrium model with deterministic price dynamics

The separation rule of the directional model classifies observations on

the demand or supply-side based in a binary fashion, which is not always

flexible, as observations that correspond to large shortages/surpluses

are treated the same with observations that correspond to small

shortages/ surpluses. The deterministic adjustment model of the package

replaces this binary separation rule with a quantitative one (Fair and

Jaffee 1972; Maddala and Nelson 1974). The magnitude of the price

movements is analogous to the magnitude of deviations from the

market-clearing condition. This model offers a flexible estimation

alternative, with one extra degree of freedom in the estimation of price

dynamics, that accounts for market forces that are in alignment with

standard economic reasoning. By letting

approach zero, the equilibrium model can be obtained as a

limiting case of this model.

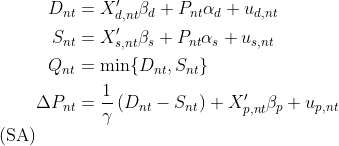

## A disequilibrium model with stochastic price dynamics

The last model of the package extends the price dynamics of the

deterministic adjustment model by adding additional explanatory

variables and a stochastic term. The latter term, in particular, makes

the price adjustment mechanism stochastic and, deviating from the

structural assumptions of models

and

, abstains from imposing any separation assumption on the sample

(Maddala and Nelson 1974; Quandt and Ramsey 1978). The estimation of

this model offers the highest degree of freedom, accompanied, however,

by a significant increase in estimation complexity, which can hinder the

stability of the procedure and the numerical accuracy of the outcomes.

## A disequilibrium model with stochastic price dynamics

The last model of the package extends the price dynamics of the

deterministic adjustment model by adding additional explanatory

variables and a stochastic term. The latter term, in particular, makes

the price adjustment mechanism stochastic and, deviating from the

structural assumptions of models

and

, abstains from imposing any separation assumption on the sample

(Maddala and Nelson 1974; Quandt and Ramsey 1978). The estimation of

this model offers the highest degree of freedom, accompanied, however,

by a significant increase in estimation complexity, which can hinder the

stability of the procedure and the numerical accuracy of the outcomes.

# Installation and documentation

The released version of

[*markets*](https://CRAN.R-project.org/package=markets) can be installed

from [CRAN](https://CRAN.R-project.org) with:

``` r

install.packages("markets")

```

The source code of the in-development version can be downloaded from

[GitHub](https://github.com/pi-kappa-devel/markets).

After installing it, there is a basic-usage example installed with it.

To see it type the command

``` r

vignette('basic_usage')

```

Online documentation is available for both the

[released](https://www.markets.pikappa.eu) and

[in-development](https://www.markets.pikappa.eu/dev/) versions of the

package. The documentation files can also be accessed in `R` by typing

``` r

?? markets

```

An overview of the package’s functionality was presented in the session

Trends, Markets, Models of the

[useR\!2021](https://user2021.r-project.org/) conference. The recording

of the session, including the talk for this package, can be found in the

video that follows. The presentation slides of the talk are also

available [here](https://talks.pikappa.eu/useR!2021/).

# A practical example

This is a basic example that illustrates how a model of the package can

be estimated. The package is loaded in the standard way.

``` r

library(markets)

```

The example uses simulated data. The *markets* package offers a function

to simulate data from data generating processes that correspond to the

models that the package provides.

``` r

model_tbl <- simulate_data(

"diseq_basic", 10000, 5,

-1.9, 36.9, c(2.1, -0.7), c(3.5, 6.25),

2.8, 34.2, c(0.65), c(1.15, 4.2),

NA, NA, c(NA),

seed = 42

)

```

Models are initialized by a constructor. In this example, a basic

disequilibrium model is estimated. There are also other models available

(see [Design and functionality](#design-and-functionality)). The

constructor sets the model’s parameters and performs the necessary

initialization processes. The following variables specify this example’s

parameterization.

- The models can be estimated both with panel and time series data.

The constructor expects both a subject and a time identifier in

order to perform the necessary initialization operations (these are

respectively given by `id` and `date` in the simulated data of this

example). The observation identification of the data is

automatically generated by composing the subject and time

identifiers. The resulting composite key is the combination of

columns that uniquely identify a record of the dataset.

- The observable traded quantity variable (given by `Q` in this

example’s simulated data). The demanded and supplied quantities are

not observable, and they are identified either based on the market

clearing condition or the short side rule.

- The price variable, which is named after `P` in the simulated data.

- The right-hand side specifications of the demand and supply

equations. The expressions are specified similarly to the

expressions of formulas of linear models. Indicator variables and

interactions are created automatically by the constructor.

- The verbosity level controls the level of messaging. The object

displays

- error: always,

- warning: ≥ 1,

- info: ≥ 2,

- verbose: ≥ 3 and

- debug: ≥ 4.

``` r

verbose <- 0

```

- Should the model estimation allow for correlated demand and supply

shocks?

``` r

correlated_shocks <- TRUE

```

The model is estimated with default options by a simple call. See the

documentation of `estimate` for more details and options.

``` r

fit <- diseq_basic(

Q | P | id | date ~ P + Xd1 + Xd2 + X1 + X2 | P + Xs1 + X1 + X2,

model_tbl, correlated_shocks = correlated_shocks, verbose = verbose

)

```

The results can be inspected in the usual fashion via `summary`.

``` r

summary(fit)

```

## Basic Model for Markets in Disequilibrium:

## Demand RHS : D_P + D_Xd1 + D_Xd2 + D_X1 + D_X2

## Supply RHS : S_P + S_Xs1 + S_X1 + S_X2

## Short Side Rule : Q = min(D_Q, S_Q)

## Shocks : Correlated

## Nobs : 50000

## Sample Separation : Not Separated

## Quantity Var : Q

## Price Var : P

## Key Var(s) : id, date

## Time Var : date

##

## Maximum likelihood estimation:

## Method : BFGS

## Convergence Status : success

## Starting Values :

## D_P D_CONST D_Xd1 D_Xd2 D_X1 D_X2 S_P

## 1.2430 32.8102 0.6986 -0.2362 1.9377 4.8826 1.2390

## S_CONST S_Xs1 S_X1 S_X2 D_VARIANCE S_VARIANCE RHO

## 32.8104 0.4500 1.9376 4.8819 3.8528 4.2008 0.0000

##

## Coefficients:

## Estimate Std. Error z value Pr(z)

## D_P -1.924718 0.013833 -139.1346 0.0000

## D_CONST 36.937193 0.021933 1684.0868 0.0000

## D_Xd1 2.110786 0.009405 224.4360 0.0000

## D_Xd2 -0.691555 0.008147 -84.8864 0.0000

## D_X1 3.521398 0.009738 361.6230 0.0000

## D_X2 6.262825 0.009397 666.4653 0.0000

## S_P 2.797103 0.007373 379.3764 0.0000

## S_CONST 34.188334 0.007529 4540.9220 0.0000

## S_Xs1 0.663960 0.005615 118.2557 0.0000

## S_X1 1.139702 0.006086 187.2806 0.0000

## S_X2 4.203214 0.005976 703.3021 0.0000

## D_VARIANCE 0.996663 0.012529 79.5456 0.0000

## S_VARIANCE 1.006628 0.008312 121.0987 0.0000

## RHO -0.009219 0.026586 -0.3467 0.7288

##

## -2 log L: 138460

# Design and functionality

The equilibrium model can be estimated either using two-stage least

squares or full information maximum likelihood. The two methods are

asymptotically equivalent. The class for which both of these estimation

methods are implemented is

- `equilibrium_model`.

In total, there are four disequilibrium models, which are all estimated

using full information maximum likelihood. By default, the estimations

use analytically calculated gradient expressions, but the user has the

ability to override this behavior. The classes that implement the four

disequilibrium models are

- `diseq_basic`,

- `diseq_directional`,

- `diseq_deterministic_adjustment`, and

- `diseq_stochastic_adjustment`.

The package organizes these classes in a simple object oriented

hierarchy.

# Installation and documentation

The released version of

[*markets*](https://CRAN.R-project.org/package=markets) can be installed

from [CRAN](https://CRAN.R-project.org) with:

``` r

install.packages("markets")

```

The source code of the in-development version can be downloaded from

[GitHub](https://github.com/pi-kappa-devel/markets).

After installing it, there is a basic-usage example installed with it.

To see it type the command

``` r

vignette('basic_usage')

```

Online documentation is available for both the

[released](https://www.markets.pikappa.eu) and

[in-development](https://www.markets.pikappa.eu/dev/) versions of the

package. The documentation files can also be accessed in `R` by typing

``` r

?? markets

```

An overview of the package’s functionality was presented in the session

Trends, Markets, Models of the

[useR\!2021](https://user2021.r-project.org/) conference. The recording

of the session, including the talk for this package, can be found in the

video that follows. The presentation slides of the talk are also

available [here](https://talks.pikappa.eu/useR!2021/).

# A practical example

This is a basic example that illustrates how a model of the package can

be estimated. The package is loaded in the standard way.

``` r

library(markets)

```

The example uses simulated data. The *markets* package offers a function

to simulate data from data generating processes that correspond to the

models that the package provides.

``` r

model_tbl <- simulate_data(

"diseq_basic", 10000, 5,

-1.9, 36.9, c(2.1, -0.7), c(3.5, 6.25),

2.8, 34.2, c(0.65), c(1.15, 4.2),

NA, NA, c(NA),

seed = 42

)

```

Models are initialized by a constructor. In this example, a basic

disequilibrium model is estimated. There are also other models available

(see [Design and functionality](#design-and-functionality)). The

constructor sets the model’s parameters and performs the necessary

initialization processes. The following variables specify this example’s

parameterization.

- The models can be estimated both with panel and time series data.

The constructor expects both a subject and a time identifier in

order to perform the necessary initialization operations (these are

respectively given by `id` and `date` in the simulated data of this

example). The observation identification of the data is

automatically generated by composing the subject and time

identifiers. The resulting composite key is the combination of

columns that uniquely identify a record of the dataset.

- The observable traded quantity variable (given by `Q` in this

example’s simulated data). The demanded and supplied quantities are

not observable, and they are identified either based on the market

clearing condition or the short side rule.

- The price variable, which is named after `P` in the simulated data.

- The right-hand side specifications of the demand and supply

equations. The expressions are specified similarly to the

expressions of formulas of linear models. Indicator variables and

interactions are created automatically by the constructor.

- The verbosity level controls the level of messaging. The object

displays

- error: always,

- warning: ≥ 1,

- info: ≥ 2,

- verbose: ≥ 3 and

- debug: ≥ 4.

``` r

verbose <- 0

```

- Should the model estimation allow for correlated demand and supply

shocks?

``` r

correlated_shocks <- TRUE

```

The model is estimated with default options by a simple call. See the

documentation of `estimate` for more details and options.

``` r

fit <- diseq_basic(

Q | P | id | date ~ P + Xd1 + Xd2 + X1 + X2 | P + Xs1 + X1 + X2,

model_tbl, correlated_shocks = correlated_shocks, verbose = verbose

)

```

The results can be inspected in the usual fashion via `summary`.

``` r

summary(fit)

```

## Basic Model for Markets in Disequilibrium:

## Demand RHS : D_P + D_Xd1 + D_Xd2 + D_X1 + D_X2

## Supply RHS : S_P + S_Xs1 + S_X1 + S_X2

## Short Side Rule : Q = min(D_Q, S_Q)

## Shocks : Correlated

## Nobs : 50000

## Sample Separation : Not Separated

## Quantity Var : Q

## Price Var : P

## Key Var(s) : id, date

## Time Var : date

##

## Maximum likelihood estimation:

## Method : BFGS

## Convergence Status : success

## Starting Values :

## D_P D_CONST D_Xd1 D_Xd2 D_X1 D_X2 S_P

## 1.2430 32.8102 0.6986 -0.2362 1.9377 4.8826 1.2390

## S_CONST S_Xs1 S_X1 S_X2 D_VARIANCE S_VARIANCE RHO

## 32.8104 0.4500 1.9376 4.8819 3.8528 4.2008 0.0000

##

## Coefficients:

## Estimate Std. Error z value Pr(z)

## D_P -1.924718 0.013833 -139.1346 0.0000

## D_CONST 36.937193 0.021933 1684.0868 0.0000

## D_Xd1 2.110786 0.009405 224.4360 0.0000

## D_Xd2 -0.691555 0.008147 -84.8864 0.0000

## D_X1 3.521398 0.009738 361.6230 0.0000

## D_X2 6.262825 0.009397 666.4653 0.0000

## S_P 2.797103 0.007373 379.3764 0.0000

## S_CONST 34.188334 0.007529 4540.9220 0.0000

## S_Xs1 0.663960 0.005615 118.2557 0.0000

## S_X1 1.139702 0.006086 187.2806 0.0000

## S_X2 4.203214 0.005976 703.3021 0.0000

## D_VARIANCE 0.996663 0.012529 79.5456 0.0000

## S_VARIANCE 1.006628 0.008312 121.0987 0.0000

## RHO -0.009219 0.026586 -0.3467 0.7288

##

## -2 log L: 138460

# Design and functionality

The equilibrium model can be estimated either using two-stage least

squares or full information maximum likelihood. The two methods are

asymptotically equivalent. The class for which both of these estimation

methods are implemented is

- `equilibrium_model`.

In total, there are four disequilibrium models, which are all estimated

using full information maximum likelihood. By default, the estimations

use analytically calculated gradient expressions, but the user has the

ability to override this behavior. The classes that implement the four

disequilibrium models are

- `diseq_basic`,

- `diseq_directional`,

- `diseq_deterministic_adjustment`, and

- `diseq_stochastic_adjustment`.

The package organizes these classes in a simple object oriented

hierarchy.

Concerning post estimation analysis, the package offers functionality to

calculate

- shortage probabilities,

- marginal effects on shortage probabilities,

- point estimates of normalized shortages,

- point estimates of relative shortages,

- aggregate demand and supply,

- post-estimation classification of observations in demand and supply,

- heteroscedasticity-adjusted (Huber-White) standard errors, and

- clustered standard errors.

# Alternative packages

The estimation of the basic model is also supported by the package

[*Disequilibrium*](https://CRAN.R-project.org/package=Disequilibrium).

By default, the *Disequilibrium* package numerically approximates the

gradient when optimizing the likelihood. In contrast, *markets* uses

analytically calculated expressions for the likelihood, which can reduce

the duration of estimating the model. In addition, it allows the user to

override this behavior and use the numerically approximated gradient.

There is no alternative package that supports the out-of-the-box

estimation of the other three disequilibrium models of *markets*.

# Planned extensions

The package is planned to be expanded in the following ways:

1. The package should become more inclusive by adding additional market

models.

2. Single-command functionality for the market-clearing tests

(e.g. (Karapanagiotis, n.d.; Hwang 1980; Quandt 1978)) should be

included in the package.

3. Alternative estimation methods (e.g. (Zilinskas and Bogle 2006;

Quandt and Ramsey 1978)) could also be implemented.

# Contributors

[Pantelis Karapanagiotis](https://www.pikappa.eu)

Feel free to join, share, contribute, distribute.

# License

The code is distributed under the MIT License.

# References

Concerning post estimation analysis, the package offers functionality to

calculate

- shortage probabilities,

- marginal effects on shortage probabilities,

- point estimates of normalized shortages,

- point estimates of relative shortages,

- aggregate demand and supply,

- post-estimation classification of observations in demand and supply,

- heteroscedasticity-adjusted (Huber-White) standard errors, and

- clustered standard errors.

# Alternative packages

The estimation of the basic model is also supported by the package

[*Disequilibrium*](https://CRAN.R-project.org/package=Disequilibrium).

By default, the *Disequilibrium* package numerically approximates the

gradient when optimizing the likelihood. In contrast, *markets* uses

analytically calculated expressions for the likelihood, which can reduce

the duration of estimating the model. In addition, it allows the user to

override this behavior and use the numerically approximated gradient.

There is no alternative package that supports the out-of-the-box

estimation of the other three disequilibrium models of *markets*.

# Planned extensions

The package is planned to be expanded in the following ways:

1. The package should become more inclusive by adding additional market

models.

2. Single-command functionality for the market-clearing tests

(e.g. (Karapanagiotis, n.d.; Hwang 1980; Quandt 1978)) should be

included in the package.

3. Alternative estimation methods (e.g. (Zilinskas and Bogle 2006;

Quandt and Ramsey 1978)) could also be implemented.

# Contributors

[Pantelis Karapanagiotis](https://www.pikappa.eu)

Feel free to join, share, contribute, distribute.

# License

The code is distributed under the MIT License.

# References